It’s clear that what buying a home looks like today has changed in the past few years. The market shift has brought about many benefits for buyers, and there are several reasons that this market is more attractive than ever to those who have considered buying but have been put off due to rising mortgage rates.

The best way to decide whether to buy a home in any particular market is to research the facts and not follow the headlines. Those headlines can be more frightening to potential buyers than they are helpful in understanding the reality of the situation.

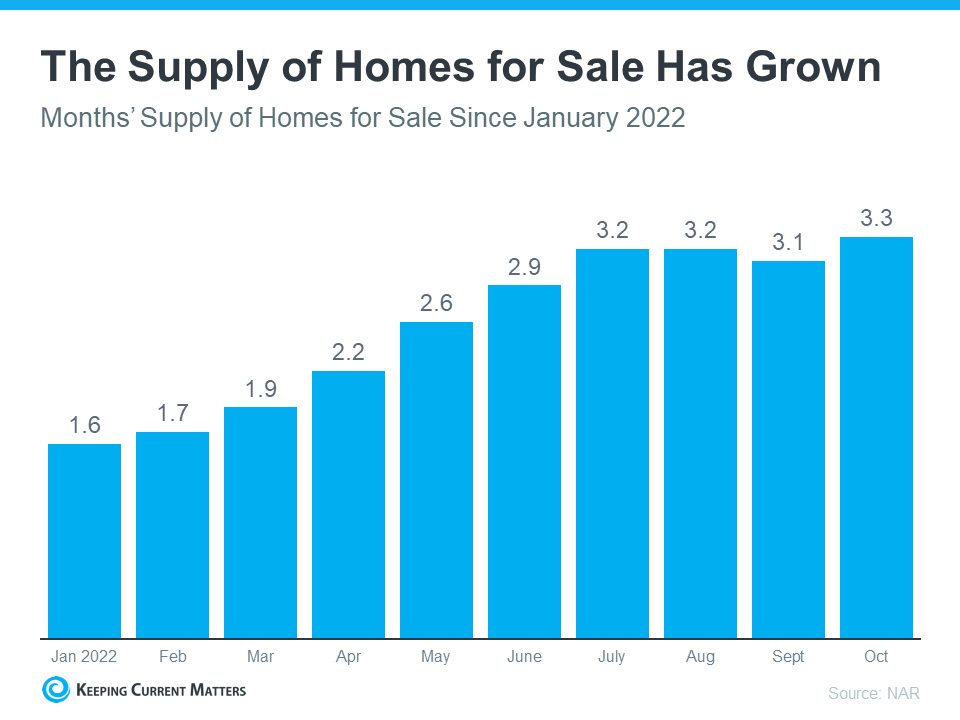

1. There are more homes for sale right now

According to the National Association of Realtors (NAR), the number of homes available for sale this year has increased significantly over the past 12 months (see graph below).

Two factors have led to this growth: homeowners are listing their homes for sale, and homes remain on the market longer due to buyer response to higher mortgage rates.

The good news is that with more inventory, you have more homes to choose from. You could also see less competition from other buyers if there are more homes available, as the peak frenzy for competing for the same house has slowed down.

Two factors have led to this growth: homeowners are listing their homes for sale, and homes remain on the market longer due to buyer response to higher mortgage rates.

The good news is that with more inventory, you have more homes to choose from. You could also see less competition from other buyers if there are more homes available, as the peak frenzy for competing for the same house has slowed down.

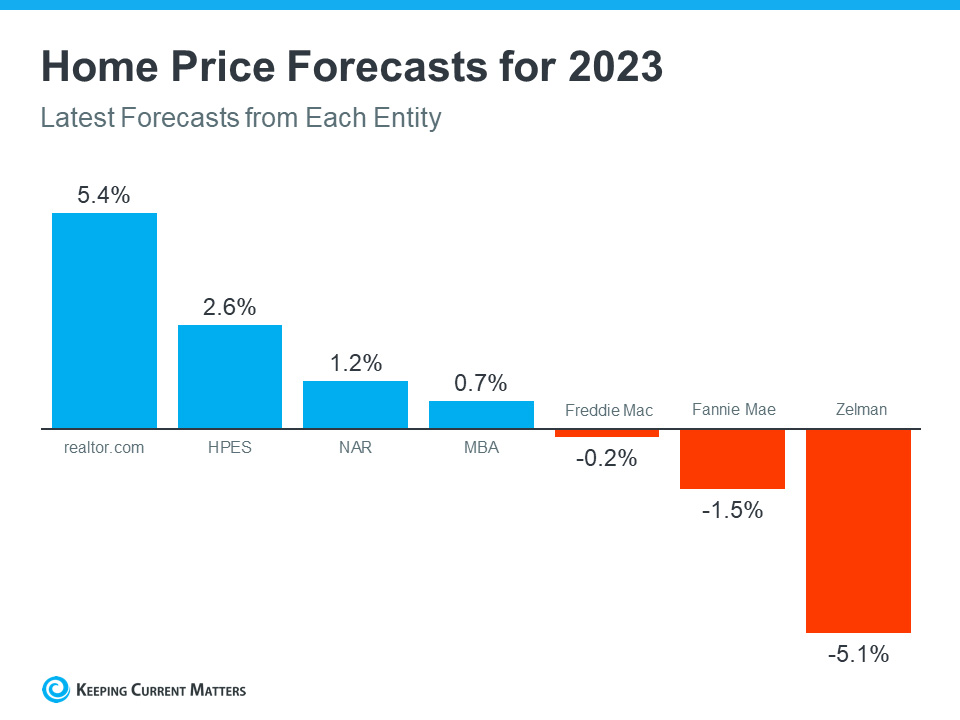

2. A Home Price Crash is Not Projected

Experts aren’t convinced that home prices will plummet as they did in 2008. Instead, they will moderate depending on local markets and factors such as supply and demand. Some experts call for slight appreciation, while others call for slight depreciation (see graph).

The expectation for next year’s price growth is relatively flat to neutral if you look at the big picture and the average expert forecasts for 2023. If you are worried about buying a house because home prices may crash, don’t be. Expert projections show that this is not the case.

The expectation for next year’s price growth is relatively flat to neutral if you look at the big picture and the average expert forecasts for 2023. If you are worried about buying a house because home prices may crash, don’t be. Expert projections show that this is not the case.

3. Although Mortgage Rates Have Risen, They Will Come Down.

Although mortgage rates have increased dramatically in the past year, they have been slowing down in recent weeks. Early signs suggest that inflation is easing. The future of inflation will determine where they go. If rates could drop if inflation really begins to slow down.

Expect more buyers to enter the market when that happens. This means that you will once again be competing with other buyers. You could be one step ahead by buying your house before other buyers enter the market. As Lawrence Yun, Chief Economist for NAR, says:

“The upcoming months should see a return of buyers, as mortgage rates appear to have already peaked and have been coming down since mid-November.”

Those who are sitting on the fence will rush back if mortgage rates drop. You have the advantage of getting in before they do.

Expect more buyers to enter the market when that happens. This means that you will once again be competing with other buyers. You could be one step ahead by buying your house before other buyers enter the market. As Lawrence Yun, Chief Economist for NAR, says:

“The upcoming months should see a return of buyers, as mortgage rates appear to have already peaked and have been coming down since mid-November.”

Those who are sitting on the fence will rush back if mortgage rates drop. You have the advantage of getting in before they do.

Bottom Line

You should consider all the benefits that today’s market has to offer when you are considering buying a house. It may be a good idea to connect with a local realtor professional in order to make homeownership possible.